As I was getting ready for work this morning, I was listening to Vermont Public Radio and an NPR story came on Morning Edition called “Is Wall Street Eating Your 401(k) Nest Egg?” This story hit home for me because we recently went through the same painful process of selecting our own 401k provider.

In the NPR story, the reporter Chris Arnold, describes how a well-meaning small company got duped into choosing an employee retirement plan where the financial advisor took literally half of each employees retirement earnings. This is an important lesson for any business considering a 401k plan.

Our own experience choosing a 401k plan

In this blog, we don’t normally cover 401k’s or anything in the realm of finance. We’re a marketing software company and this is not our typical area of expertise. So, don’t take this article as financial advice or as well-researched as the NPR story. I just want to share our own experience and the data we gathered in the process of choosing our own 401k program.

Back in July, we implemented our own 401k for our employees. This was after six months of review of the plans available. This also was after many years of false starts getting a retirement plan in place. Finally, after 15 years in business, we finally have a retirement plan for our employees.

The mirror world of finance is confusing even for the savviest finance person. Fortunately, our director of finance, Joanne, had some experience with choosing a 401k program. She guided the company through the treacherous waters. But even with her prior experience, it was a challenging process that required diligence at every step along the way.

The 401k plan you choose makes a HUGE difference for your employees retirement savings

Although we started with some of the better programs and did not consider high fee programs, we discovered a huge range of fees from 401k Plan Providers. The annual fees ranged from 0.055% of assets to 1.1% of assets. The example in the NPR story was 2% of assets, which is well above any that we actively considered, but certainly in the range of the ones in the initial consideration set.

We found the best 401k plan delivers 72% higher returns than the worst

These small percentages on fees don’t sound like a lot, but they make a huge difference in returns over the lifetime of your 401k contributions. Consider the following example employee:

- $100,000 salary

- 4% employee contribution

- 4% employer match (typical of safe harbor plan)

- 5% rate of return on investment (right in the middle of the 5-8% expected range)

- 25 year contribution period

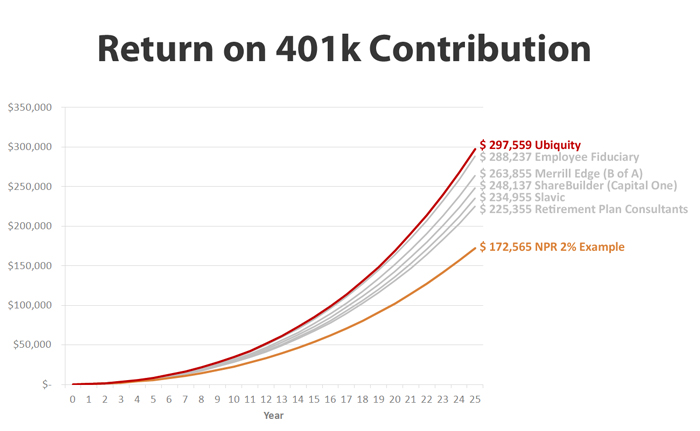

Based on this example and the plans we evaluated plus the NPR example from this morning’s story, you find a huge variation in returns for this employee. Choosing the right plan makes a difference of $125,000 in their retirement savings. The best plan from Ubiquity delivers 72% higher returns than the worst plan based on fees alone.

Here are the summary numbers based on the vendors we evaluated:

And here’s what the returns look like over time:

It’s painful, but do your homework when choosing your 401k

Based on Joanne’s careful analysis, we ended up going with Ubiquity. We’re only a few months in, but I’m happy to report that so far their service has been good. Now, if only the stock market would cooperate!

My recommendation for anyone choosing a 401k plan is to follow Joanne’s lead and the advice in the NPR story: do the right thing for your employees. It’s not a fun job, but you need to do your homework on 401k plans. It makes a huge difference.

Here’s the NPR story. It’s worth a listen: